How to Manage Restaurant Cash Flow (Without Losing Sleep)

A practical guide to restaurant cash flow management — covering the timing mismatches, seasonal swings, and vendor payment cycles that catch operators off guard.

Most restaurants don't fail because they're unprofitable. They fail because they run out of cash.

The distinction matters. Your P&L might show a healthy margin for the month, but if your bank balance hits zero before rent is due on the first, profitability won't save you. The restaurant industry has a built-in timing problem: customers pay immediately, but your costs arrive on different schedules — vendor invoices due in 7-30 days, payroll every week or two, rent on the first, insurance quarterly.

Managing cash flow well means seeing these timing mismatches before they become emergencies.

Why Restaurant Cash Flow Is Different

Every business deals with cash flow, but restaurants have specific dynamics that make it harder:

Credit card settlement lag. Most restaurant revenue comes through credit cards, which take 1-3 business days to settle. A strong Friday night doesn't fund Monday's produce delivery. During high-volume periods, this daily float can create a gap of $5,000-$15,000 between what you've earned and what's in your account.

Perishable inventory on tight cycles. You can't stock up on produce when cash is flush — it'll spoil. Food costs arrive as frequent, small purchases (daily or every-other-day deliveries) that add up to 28-35% of revenue. Unlike a retailer who can time inventory purchases, your purchasing cycle is dictated by shelf life. The restaurant inventory management best practices guide covers par levels and ordering rhythms that keep cash outflows predictable.

Labor costs are fixed in the short term. You can't cut Tuesday's prep cook because Monday was slow. Payroll runs on a fixed weekly or bi-weekly cycle regardless of recent sales. For most restaurants, labor runs 25-35% of revenue, and it hits your bank account on a predictable schedule.

Seasonal revenue swings. Many restaurants see 25-40% variation between their best and worst months. A restaurant that's flush in December may be genuinely tight in February. Without a cash flow projection, these swings catch operators off guard. Building a restaurant sales forecast with seasonal multipliers makes these swings visible months in advance.

The 13-Week Cash Flow Projection

The most useful planning horizon for restaurant operators is 13 weeks — one quarter. It's long enough to see upcoming cash crunches and short enough to forecast with reasonable accuracy.

Here's what a 13-week projection should track:

Cash inflows (by week)

- Dine-in sales (net of credit card settlement timing)

- Takeout and delivery revenue

- Catering deposits and event revenue

- Alcohol sales (if tracked separately)

- Gift card redemptions

- Any other income (merchandise, cooking classes)

Cash outflows (by timing)

- Daily/weekly: Food and beverage vendor deliveries, produce orders

- Weekly/bi-weekly: Payroll (hourly staff, management, employer taxes, tips)

- Monthly: Rent, utilities, insurance, POS/technology fees, marketing

- Irregular: Equipment repairs, permit renewals, quarterly insurance premiums, loan payments

The projection calculates ending cash balance week by week. When you see a week where the balance drops below your minimum operating threshold (typically 2-4 weeks of expenses), you have 3-6 weeks to act.

What to Do When Cash Gets Tight

A cash flow projection is only useful if you act on what it shows. When you see a tight week coming:

-

Negotiate vendor timing. Call your broadline distributor and ask to push a payment from net-7 to net-14 for one cycle. Most suppliers will accommodate a request like this once or twice per year, especially for accounts in good standing.

-

Accelerate inflows. If you have a catering deposit coming, invoice it earlier. If you're running a gift card promotion, launch it now instead of next month.

-

Draw on your line of credit proactively. If you have a credit line, draw before the rate changes or before you actually need it. A planned draw at a known rate is better than an emergency scramble.

-

Defer discretionary spending. That kitchen equipment upgrade or marketing campaign can wait two weeks. Non-essential purchases are the easiest lever to pull.

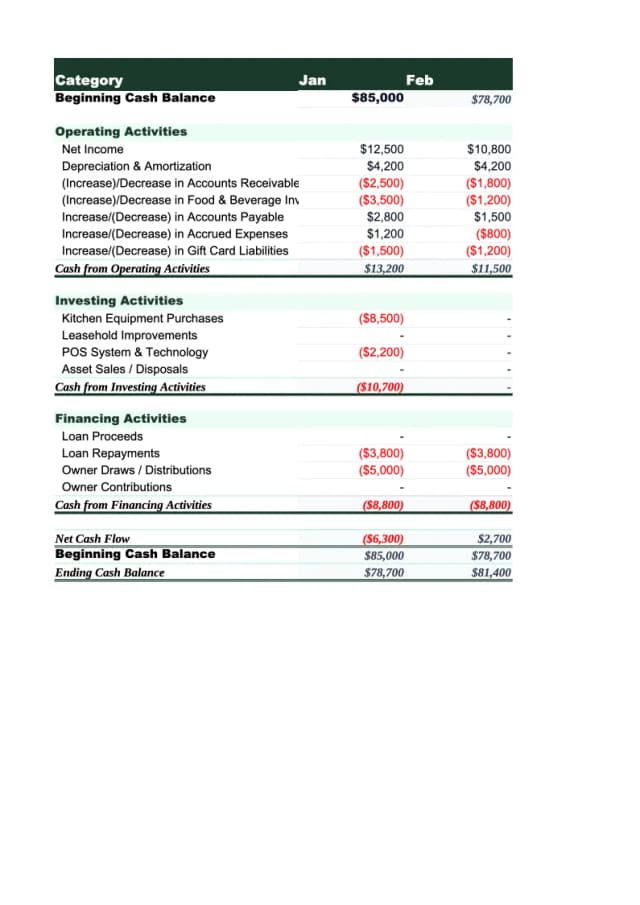

Monthly Cash Flow for Lenders and Investors

The weekly view is your operational tool. But banks, SBA lenders, and investors want to see a monthly cash flow statement — typically 12 months historical plus 12 months projected.

The standard format separates cash flows into three categories:

- Operating activities: Cash from customers minus cash to suppliers, employees, and operating expenses

- Investing activities: Equipment purchases, renovation costs, proceeds from asset sales

- Financing activities: Loan draws, repayments, owner contributions, distributions

This is the format you'll share when applying for an SBA loan, negotiating a lease, or bringing on an investor. Having it ready — rather than scrambling to build it when the bank asks — signals that you're running a serious operation.

If you want a pre-built version of this, the Restaurant Cash Flow Template includes both the weekly and monthly views with restaurant-specific categories already set up.

Need a ready-made cash flow template for your restaurant?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Handling Seasonality

The biggest cash flow mistake restaurant operators make is planning with averages. If your average monthly revenue is $120,000, it's tempting to budget $120,000 every month. But if December does $160,000 and February does $85,000, the average is irrelevant — you need to plan for the $85,000 month.

A seasonality adjustment works like this:

- Look at your last 12 months of POS data

- Calculate each month's revenue as a percentage of the annual average

- Apply those percentages to your forward projection

If January historically runs at 75% of average, your January cash flow projection should use 75% of average revenue — not the actual average. This single adjustment prevents most seasonal cash surprises.

For restaurants without 12 months of history, industry benchmarks are a reasonable starting point. Most full-service restaurants see peaks in May-June (patio season) and November-December (holiday dining), with troughs in January-February and sometimes August.

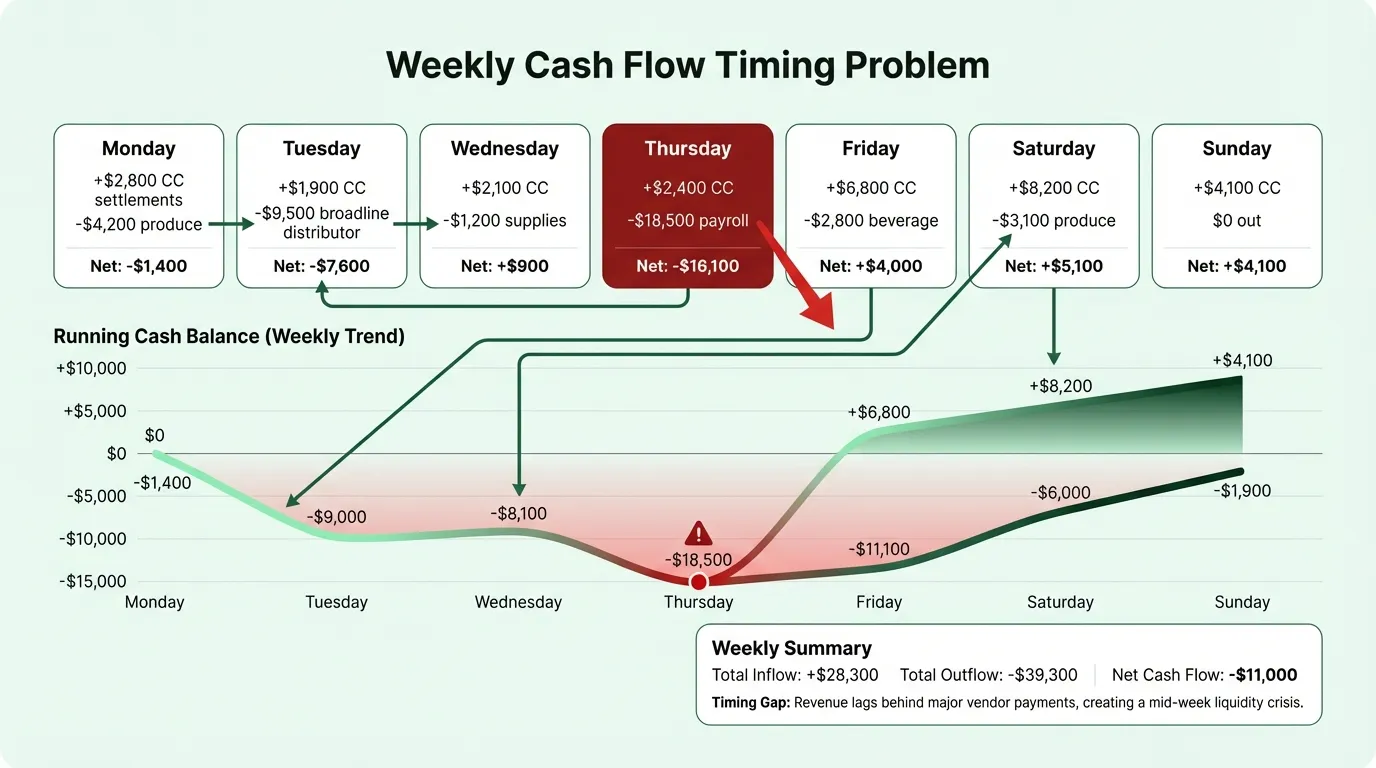

The Vendor Payment Calendar

One pattern that catches even experienced operators: multiple large vendor invoices falling due in the same week.

Your broadline food distributor, beverage vendor, and linen service may all invoice on similar cycles. When three $3,000-$5,000 invoices hit the same week as payroll, you get a $15,000-$25,000 cash outflow that looks alarming even if the monthly total is normal.

The fix is a vendor payment calendar — a simple tracker listing each vendor, their typical invoice amount, payment terms, and payment frequency. When you can see that three major vendors all invoice in week 2 of each month, you know to hold extra cash going into that week.

You can also use this calendar to stagger payment timing. If your distributor is on net-7 and your beverage vendor is on net-14, you naturally spread cash outflows. But if both are on net-7 from the same invoice date, consider negotiating different terms with one. The restaurant cash flow calculator lets you model how shifting a single vendor's payment terms changes your weekly cash position.

Tools for the Job

You don't need specialized software for restaurant cash flow management. A well-built spreadsheet is the right tool for most independent restaurants and small chains. The key requirements:

- 13-week rolling view with restaurant-specific inflow and outflow categories

- Monthly view in the format banks and lenders expect

- Seasonality adjustment so projections reflect your actual revenue patterns

- Vendor payment tracker to catch payment clustering

The Restaurant Cash Flow Template covers all four. If you're also tracking profitability, the Restaurant Budget Template and Restaurant P&L Template complement the cash flow view — profit tells you if you're making money, cash flow tells you if you can pay your bills.

The Weekly Review Habit

The operators who manage cash well share one habit: they spend 15 minutes every Monday updating their projection.

The process is simple:

- Enter last week's actual sales and payments

- Roll the 13-week window forward one week

- Check whether any upcoming week's ending balance falls below your minimum threshold

- If it does, take one of the four actions above

That's it. Fifteen minutes a week eliminates most of the financial surprises that put restaurant operators in crisis mode. The projection won't be perfectly accurate — some weeks will be better than expected, some worse — but the trend is what matters. If your ending cash balance is trending downward over 4-6 weeks, you need to act before it becomes an emergency.

Cash flow management isn't complicated. It's just a habit most restaurant operators never build because they're focused on the kitchen, the floor, and the next service. But the operators who do build it say the same thing: once you start, you wonder how you ever ran the business without it.

Last updated: March 23, 2026

Frequently Asked Questions

Related Articles

Construction Cash Flow Example: How It Actually Works

A real-world construction cash flow example showing how retainage, draw schedules, and payment delays create cash gaps — and how to plan around them.

Hotel Cash Flow Example: Why Occupancy Doesn't Equal Cash

A real hotel cash flow example covering OTA commission timing, advance deposits, RevPAR gaps, and how to build a projection that prevents off-season surprises.

Restaurant Cash Flow Example: Real Numbers, Real Format

A complete restaurant cash flow example with real benchmark numbers — monthly statement, weekly view, and what each line actually means for your operation.