Real Estate Accounting: A Practical Guide for Investors

Real estate accounting has rules that trip up even experienced investors. This guide covers depreciation, Schedule E, passive losses, 1031 exchanges, and the mistakes that cost money.

Real estate accounting follows the same foundational rules as any business accounting — but several features of real property make it work differently in practice. Get the structure right and you have a clear picture of performance, a solid tax position, and financials that hold up to lender scrutiny. Get it wrong and you'll overpay taxes, miss deductions, or discover surprises at the closing table.

How Real Estate Accounting Differs from Standard Bookkeeping

The core difference: in most businesses, fixed assets are supporting infrastructure. In real estate, land and buildings are the business. That shifts where the accounting complexity lives.

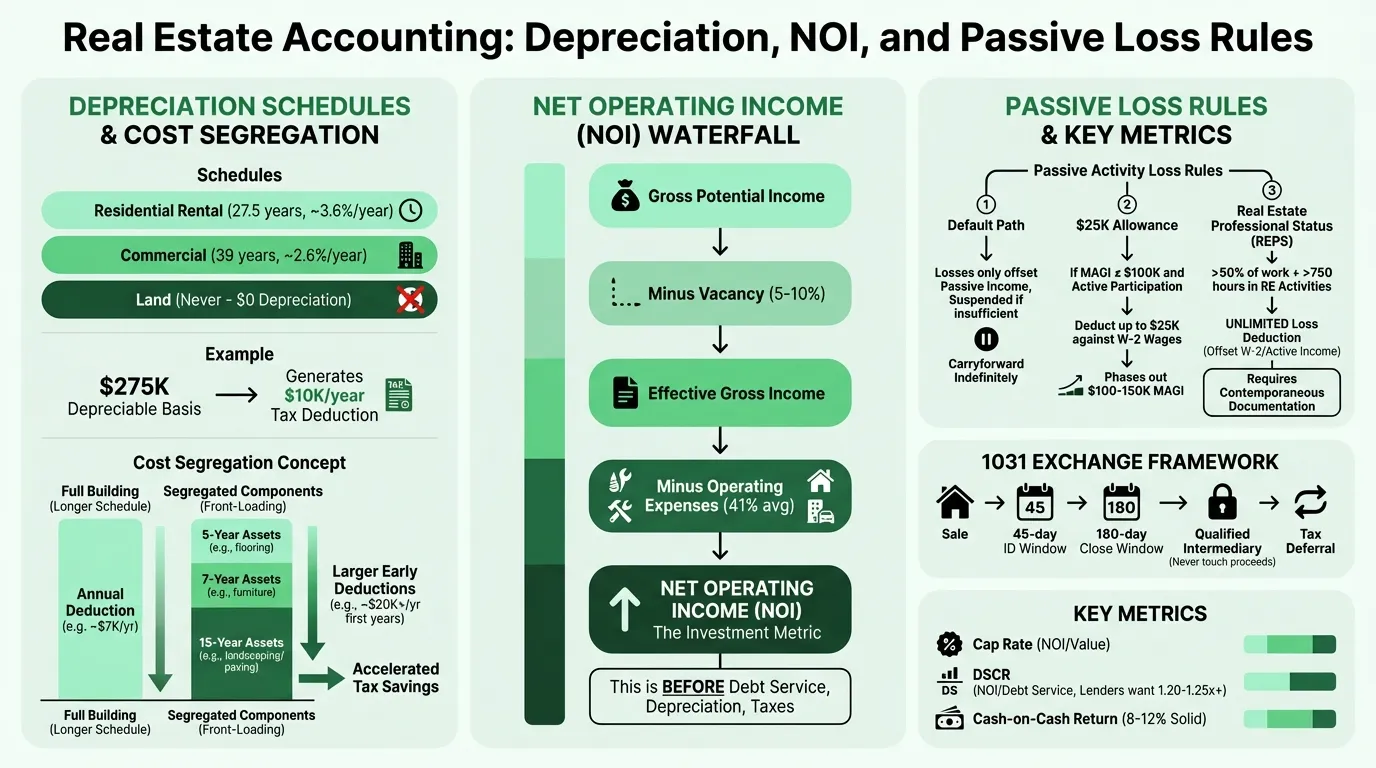

Land and buildings are split, not pooled. At acquisition, the purchase price must be allocated between land and building. Only the building depreciates — land carries no depreciation. The allocation is typically based on county assessor ratios or a formal appraisal. Getting this split wrong affects every year's tax return going forward.

The income statement stops at NOI. A real estate operating statement is structured as: Gross Potential Income → Vacancy → Effective Gross Income → Operating Expenses → Net Operating Income. Debt service, depreciation, and income taxes appear below NOI or on separate schedules. This is because those items vary by the investor's financing, not the property's performance. NOI is the standard unit of comparison.

Book value and market value diverge permanently. A property bought for $400,000 in 2015 still appears on the balance sheet at cost minus accumulated depreciation — even if its current market value is $700,000. For investors who've held properties for years, this creates a gap between book equity and economic equity that grows over time.

Security deposits are liabilities, not income. Refundable security deposits received from tenants are recorded as a balance sheet liability until returned or legally forfeited. This is explicit in IRS Publication 527: do not include security deposits in income if you may be required to return them. Many landlords make the mistake of treating deposits as revenue when collected.

Each property is its own profit center. A portfolio of five properties requires per-property tracking of income and expenses — not a single pooled rental account. You need to know which properties are performing and which are not. This is structurally similar to job costing in construction.

Depreciation: The Central Tax Benefit

Depreciation is the largest tax benefit in real estate investing, and it's also where most accounting errors occur.

Depreciation schedules by property type:

| Property Type | Useful Life | Annual Rate |

|---|---|---|

| Residential rental (building only) | 27.5 years | ~3.6% of building basis |

| Commercial real estate | 39 years | ~2.6% of building basis |

| Land | Never | $0 |

A building with $275,000 in depreciable basis (after land allocation) generates $10,000 per year in straight-line depreciation for a residential rental. That deduction reduces taxable income without a corresponding cash outflow — which is why investors call it a "paper loss." To see how depreciation accumulates on the asset side, the real estate balance sheet example walks through the contra-asset treatment line by line.

Cost segregation. A cost segregation study is an engineering analysis that reclassifies portions of a building from the 27.5 or 39-year schedule into 5-, 7-, or 15-year categories. Carpeting, certain fixtures, parking lots, and some building systems often qualify for shorter lives. Combined with bonus depreciation — reinstated at 100% for assets placed in service after January 19, 2025 under recent tax legislation — this can dramatically front-load year-one deductions.

Cost segregation is typically worth the study cost ($5,000–$15,000) for properties with a depreciable basis of $500,000 or more.

The depreciation recapture trap. Investors who sell a property that they never depreciated still owe depreciation recapture tax. The IRS taxes depreciation "allowed or allowable" — meaning you owe recapture whether you took the deduction or not. Not claiming depreciation produces the worst outcome: higher taxes every year, plus full recapture at sale. Depreciation recapture on residential rental property is taxed at a maximum rate of 25% on the recaptured amount — not at long-term capital gains rates.

Capital Improvements vs. Repairs

This classification determines whether a cost is immediately deductible or capitalized and depreciated. The stakes are real in both directions: over-capitalizing repairs inflates the asset base and misses current deductions; expensing capital improvements understates the asset basis and creates audit risk.

The IRS Tangible Property Regulations provide the governing framework using a BAR analysis:

- Betterment: Fixes a pre-existing defect, expands the property, or materially increases capacity or quality

- Adaptation: Converts the property to a new use

- Restoration: Rebuilds to like-new condition, replaces a major structural component, or restores after a casualty

If a cost meets any BAR criterion, it is a capital improvement. If not, it is a repair. Run the numbers on any renovation through our real estate break-even calculator to see whether the improvement pays for itself at your current rents.

Repairs (immediately deductible): Patching a roof leak, repairing a broken window, replacing a failed appliance with a like-kind unit, repainting an existing surface.

Capital improvements (capitalized): Replacing the entire roof, replacing all HVAC equipment, adding a bathroom, converting garage space to living area.

The analysis applies at the building system level, not just the whole structure. Replacing the entire HVAC system is likely a capitalized restoration; replacing a failed HVAC component is likely a repair.

Three safe harbors for smaller investors:

- De minimis safe harbor: Immediately deduct items costing $2,500 or less per item or invoice (without audited financials). Make the annual election on your tax return.

- Routine maintenance safe harbor: Recurring activities that keep property in efficient operating condition are deductible even if they might otherwise qualify as improvements.

- Small taxpayer safe harbor: If annual gross receipts are $10 million or less and the building's unadjusted basis is $1 million or less, deduct repairs, maintenance, and improvements totaling the lesser of $10,000 or 2% of the building's basis per year.

Schedule E and Passive Activity Loss Rules

All rental real estate income and expenses for individual investors flow through Schedule E — not Schedule C, which applies to active business income. Each property gets its own section. Gross rents, then every deductible expense (depreciation, mortgage interest, property taxes, insurance, repairs, management fees), arriving at net income or loss per property.

The passive activity problem. By default, rental real estate is a passive activity under IRC Section 469 — even if you actively manage the property. Passive losses can only offset passive income. They cannot offset W-2 wages or active business income. Passive losses that can't be used in the current year are suspended and carried forward indefinitely.

The $25,000 special allowance. There is an important exception: if your Modified Adjusted Gross Income is $100,000 or below and you actively participate in managing the property (making management decisions, approving tenants, approving repairs), you can deduct up to $25,000 in rental losses against non-passive income. This phases out between $100,000 and $150,000 MAGI and disappears entirely above $150,000.

Real estate professional status (REPS). Investors who qualify as real estate professionals under IRC Section 469(c)(7) remove rental real estate from passive activity classification entirely — allowing unlimited rental losses to offset any income. Two tests must both be met in the same year:

- More than 50% of all personal services performed during the year are in real property trades or businesses in which you materially participate

- More than 750 hours of services during the year are performed in qualifying real estate activities

For most W-2 employees, the 50% test makes REPS impossible — if you work 2,000 hours at a non-real-estate job, you'd need more than 2,000 hours in real estate. One common approach for two-income households: the spouse who manages the portfolio full-time qualifies based on their own hours.

REPS documentation is non-negotiable. The IRS scrutinizes these claims heavily. Courts have ruled against taxpayers who estimated hours retroactively. Contemporaneous daily or weekly logs documenting when, where, and what work was performed are required. Without them, REPS claims routinely fail on audit.

Need a ready-made p&l template for your real estate?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

1031 Exchanges

A 1031 exchange allows investors to defer capital gains taxes on the sale of investment property by rolling proceeds into a replacement property of equal or greater value. The gain isn't forgiven — it's deferred until the replacement property is eventually sold in a taxable transaction.

Key rules:

- Only real property qualifies (personal property exchanges ended after 2017)

- Property must be held for investment or business use — primary residences and fix-and-flip inventory do not qualify

- 45-day identification window: From the relinquished property's closing date, you have 45 calendar days to formally identify replacement properties. No exceptions outside federally declared disasters.

- 180-day closing window: Must close on replacement property within 180 calendar days of the sale, or by the tax filing deadline (with extensions) — whichever comes first. The 45-day and 180-day clocks run concurrently.

- Qualified intermediary required: The sale proceeds must go directly to a qualified intermediary — never to you. Self-dealing disqualifies the exchange entirely.

- Boot: If the replacement property costs less than the relinquished property's sale price, the difference (called "boot") is taxable in the year of the exchange.

Missing the 45-day or 180-day deadline by even one day disqualifies the exchange — there are no grace periods except for federally declared disaster relief. This is an area where accounting and deal execution need to be coordinated from day one.

The Financial Statements Real Estate Investors Need

Operating statement (income statement). Structured around NOI. Key items that landlords often omit: vacancy allowance (5–10% of gross potential income, even for currently occupied properties), capital expenditure reserves ($250–$500 per unit per year for multifamily, or 5–10% of gross income as a general benchmark), and management fees (include an 8–12% fee even if self-managing, for accurate lender-ready projections). When presenting these statements to lenders, Deckary builds consulting-grade slides.

IREM's 2023 Income/Expense data covering more than 900,000 units found that conventional multifamily properties averaged an Operating Expense Ratio of 41%. Single-family rentals typically run higher — 50–70% — due to lower economies of scale.

Balance sheet. Real estate-specific line items that differ from standard business balance sheets: land and buildings (split, with buildings net of accumulated depreciation), security deposits held (a liability — tenant money, not yours), unearned rent (advance rents already collected), and mortgages split between current portion (next 12 months' principal, from the amortization schedule) and long-term.

The Real Estate Balance Sheet Template is structured with these property-specific categories already in place.

Cash flow statement. Where the NOI-to-actual-cash gap becomes visible. Depreciation adds back (non-cash expense that reduced net income), mortgage principal payments are financing activities, and capital expenditures are investing activities. A property with strong NOI but heavy debt service can show negative cash flow after financing — investors who track only the income statement miss this.

For a deeper walkthrough of what each line item looks like, the Real Estate Balance Sheet Example and Real Estate Income Statement Example show the structure in context.

Key Metrics to Track

| Metric | Formula | What It Tells You |

|---|---|---|

| Cap Rate | NOI / Current Market Value | Property yield at current pricing |

| DSCR | NOI / Annual Debt Service | How comfortably NOI covers loan payments |

| Cash-on-Cash Return | Annual pre-tax cash flow / Equity invested | Current-year cash yield on invested capital |

| OER | Operating expenses / Gross income | What fraction of income is consumed by operations |

| Vacancy Rate | Units unoccupied / Total units | Leasing performance vs. plan |

Lenders typically require a minimum DSCR of 1.20x–1.25x for commercial real estate financing. Strong DSCR for best pricing is 1.35x or higher. Cash-on-cash returns of 8–12% are generally considered solid for stabilized income property. For a full walkthrough of how these metrics feed into deal evaluation, see the real estate financial model example.

Common Accounting Mistakes

Commingling personal and business finances. Using a personal checking account for rental income and expenses creates unreliable bookkeeping, undermines LLC liability protection, and creates audit risk. Each entity — and ideally each property — should have its own operating bank account. Security deposit accounts must be separate from operating accounts in most states by law.

Treating security deposits as income. Recording refundable deposits as rental income overstates income, overstates taxes, and understates liabilities. The correct treatment: liability when received, income only when legally forfeited. The reverse error — recording a returned deposit as an expense — is equally wrong.

Not tracking expenses by property. Running a single "rental expenses" account across a portfolio makes Schedule E preparation inaccurate and hides which properties are actually performing. The Real Estate Income Statement Template is structured for per-property tracking.

Claiming depreciation on land. The full purchase price cannot be depreciated — land has no depreciable basis. Allocate the purchase price between land and building at acquisition and document it.

Missing advance rent timing. Collecting January rent in late December? Under cash basis, that is taxable income in December. Collecting last month's rent at lease signing? That is advance rent, taxable in the year received. Many landlords incorrectly defer these amounts.

Ignoring passive loss limits. Investors above $150,000 MAGI who don't qualify as real estate professionals cannot deduct rental losses against W-2 income. Losses are suspended until there's passive income to offset them, or until the property is sold. Planning around this — either through REPS qualification or structuring income levels — is one of the highest-value decisions for high-income investors.

REPS without documentation. Qualifying as a real estate professional without contemporaneous hour logs is a claim the IRS routinely rejects on audit. Courts consistently rule against taxpayers who reconstructed hours after the fact. If you're pursuing REPS status, the logs must be kept in real time.

Setting Up the Books

The structural requirements are the same whether you use QuickBooks, Stessa, AppFolio, or a spreadsheet:

Separate accounts per property. The accounting system must produce a per-property income and expense report. This is the foundation of useful real estate accounting and accurate Schedule E preparation.

Land and building split on the asset schedule. Set up separate fixed asset accounts for land (no depreciation) and buildings (depreciation schedule in place), and track capital improvements separately with their own depreciation lives.

Security deposit liability accounts. Set up a "Security Deposits Held" liability account for each property. Tenant deposit activity should never touch the income or expense accounts unless the deposit is legally forfeited.

Mortgage amortization. Import or build a full amortization schedule for each loan so you can correctly split principal between current and long-term liabilities, and separate principal from interest (principal is a balance sheet movement; interest is an income statement expense).

Capital expenditure tracking. Maintain a running log of capital improvements with acquisition date, cost, useful life, and depreciation method. This schedule feeds Form 4562 and is essential when you sell the property and calculate gain.

Real estate accounting rewards discipline. The investors who track each property carefully — separate accounts, accurate depreciation schedules, documented cost classifications — consistently make better decisions, pay the right amount of taxes (not more), and face fewer surprises at refinancing or sale.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.